An emergency fund gives you a financial cushion for unexpected expenses.

What would happen if your car gets totaled in a crash?

Or you or a loved one gets sick or injured?

Or you’re fired from your job?

Okay I’ll stop trying to give you an anxiety attack. The point is you need to have money to provide for those moments.

People often don’t factor in unexpected purchases into their financial plan. Nobody ever expects their car to break down or for them to fall seriously ill.

Most Americans wouldn’t be able to cover a $500 surprise expense. So if you are one of the four in ten people who do have an emergency fund, you’re ahead of the majority of people AND you’re better positioned for unexpected purchases.

If you don’t have the cash, don’t worry. You’ve come to the right place. I’m going to give you a system to create an emergency fund passively AND show you when exactly to use the money.

What is an emergency fund?

An emergency fund is money saved for any unexpected expenses. The actual amount varies from person to person — but it should contain enough money for three to six months of living expenses.

More importantly, though, it gives you the peace of mind knowing you have a hedge against the worst financial disasters AND allows you to be more aggressive in other areas of your life (e.g., investing, starting a side hustle).

There are two situations where you’ll be glad you have that emergency fund:

- Surprise expenses

- Loss of income

Let’s walk through each to see what they might look like.

Unexpected expenses

Did you know that 10% of Americans took a “hardship withdrawal” from their 401k in 2015?

That means they had to withdraw money from their retirement fund, incur a hefty penalty for it, and slow their retirement plans because they didn’t have money for emergencies.

Think about that: 10% of Americans had to put off their retirement goals because they did not have an emergency fund. Your 401k and other retirement accounts should be money saved for your financial future — not to be used for unexpected expenses like:

- Medical bills

- Financial/identity theft

- Car repairs

- Home repairs

- Economy crashes

Let’s be honest: You can’t always choose whether to dip into things like credit cards or your retirement during emergencies — and that’s okay! As the wise proverb goes: Shit happens.

BUT you can anticipate the unexpected by starting an emergency fund today. Doing so will soften the impact of major financial emergencies you may encounter.

Loss of income

No one ever “plans” to lose their jobs BUT it happens. If it does happen to you, you need to be able to support yourself and your loved ones.

That’s why I recommend you have three to six months of living expenses in the bank for these situations.

The average duration for unemployment in the U.S. is just a little more than five months (per Bureau of Labor Statistics). I have six months of cash for this very reason. I know. I know. I’m the CEO of a personal finance company, how could anything go wrong? *knocks on wood*

This money provides me with peace of mind because I know I’ll be able to withstand the pressure if I ever need to use it.

How to start an emergency fund

Putting money towards an emergency fund is an AWESOME goal to have. But let’s be candid, it might take a while depending on how much you can put away each month.

For instance, if your expenses are $1,000 a month and you can only put away $50 a month towards your emergency fund, it’s going to take you ten years to save enough to have six months in the bank.

There’s one thing I want you to know: That’s okay! 57% of Americans have less than $1,000 in their savings account. That means if you save anything at all, you’re putting yourself in a better financial position than the vast majority of people.

Your emergency fund is going to take a long time to build. That’s why I’m going to show you how to build your emergency fund AND earn more money so you can finish your goal sooner. There are four steps to get there.

Step 1: Find out how much you need

First we need to know how much you need in your emergency fund.

To do that, you have to add up three to six months’ worth of:

- Utility bills (internet, water, electricity, etc.)

- Rent

- Car/home payments

- Food/groceries

- Whatever

Basically, any living expense that you have should be accounted for. Add them all up and you’ll have a rough estimate of how much you need. It’s okay if it’s not perfect. A ballpark figure will work.

Here’s a quick table that’ll show you how much you’ll need based on potential expenses:

|

MONTHLY EXPENSES |

EMERGENCY FUND (3 – 6 MONTHS) |

|

$500 |

$1,500 – $3,000 |

|

$1,000 |

$3,000 – $6,000 |

|

$2,000 |

$6,000 – $12,000 |

|

$3,000 |

$9,000 – $18,000 |

|

$4,000 |

$12,000 – $24,000 |

|

$5,000 |

$15,000 – $30,000 |

The average yearly expenses for Americans total $57,311 — or about $4,776 a month. So that means you should save about $14,328 to $28,656.

TIP: If your goal was to save up $14,328 and you were putting away $500 a month towards your goal, it’d take over two years to get there. Like I said, this is going to take a while — but I’ll show you how you can start saving easily with a great system.

When it comes time to use your emergency fund, you’re likely going to have to make some sacrifices, ESPECIALLY if you just lost your job.

This means you might have to cancel things like cable, Netflix, Uber/Lyft rides, gym memberships, and that recurring reservation at your favorite caviar fried chicken place.

“But Ramit! That goes entirely against your Rich Life philosophy! Why shouldn’t I be able to buy a latte with my emergency fund?”

Listen, there’s nothing stopping you from using your emergency money while living the lifestyle you want. You just have to factor that into your savings goals.

At the end of the day, this is your emergency fund. You can put as little or as much in it as you want. Just know that this money is there to get you through some of the toughest financial disasters of your life.

Maybe you’re content living at 70% of your current expense. Maybe nothing less than 100% is acceptable. Either works, just put away your money accordingly. When those moments happen, sacrifice might very well become necessary.

Once you know how much you roughly need to get you through three to six months, it’s time to open an account where your money will live.

Step 2: Open an account

There are two places you can put your emergency fund:

- A checking account

- A savings account

There are pros and cons to each. If your money is in a checking account, it can be more readily available for when emergencies happen. However, it can also be much easier to dip into your emergency fund for NON-emergencies because of your limited willpower.

You might prefer then to put your emergency fund in a high-yield savings account. There it can safely sit until your rainy day (and the government will insure your cash up to $250,000).

One suggestion: Find a bank that allows you to have a sub-savings account too.

This is an account you open along with your regular savings/checking accounts that can be used for specific expenses. Chances are your bank already does this. If your bank doesn’t, that’s okay! You just need to find one that does.

Here are a few great suggestions for banks that offer great savings accounts (with sub-savings):

- Capital One 360 / ING Direct (This is the one I use)

- Ally Bank

- Barclays Online

- Discover Online Savings

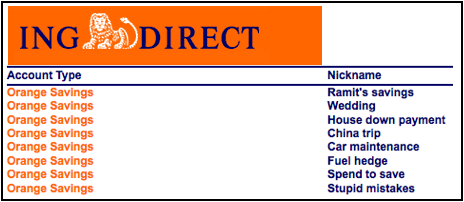

Your bank might even allow you to give the account a nickname. This lets your sub-savings accounts reflect your savings goals.

Check out all the different sub-savings accounts I had in my old savings account.

ING Direct is now Capital One 360. BTW that wedding one is going to be put to good use.

Here’s a look at a few sub-savings accounts I have now:

ING switched to Capital One 360, and I used the money I saved to buy an engagement ring

So create one and name it “Emergency Fund.” Once you have your account, it’s time to start putting away money using an automated system.

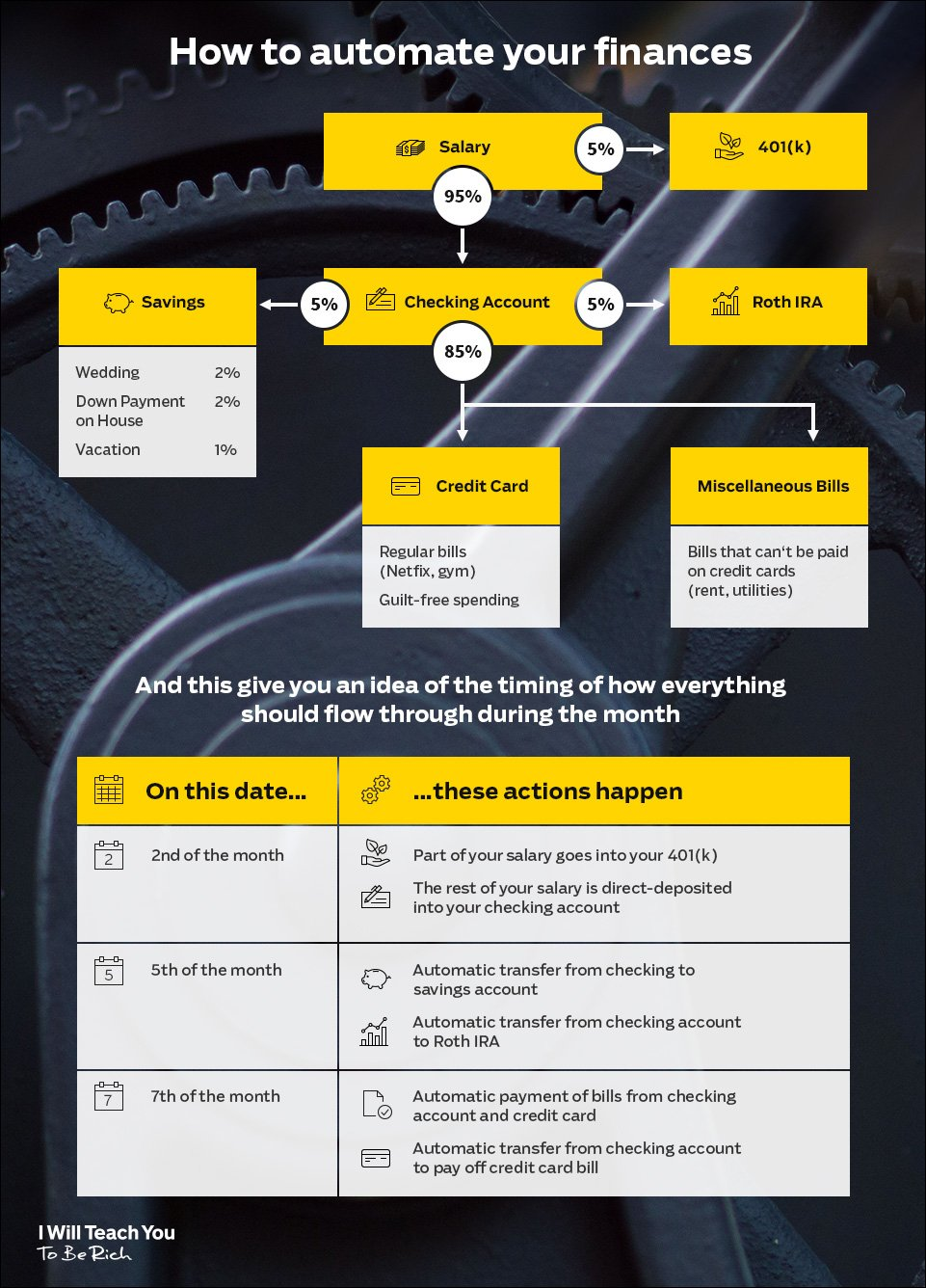

Step 3: Automate your emergency fund

Automated finances are the ultimate cure to never knowing how much you have in your checking account and how much you can spend.

When you receive your paycheck, your money is funneled to exactly where it needs to go.

Check out my video below to learn exactly how to set it up today.

I recommend you automate your accounts so you’re sending around 5% of your income into your emergency fund.

Knowing how much you’re putting in each month also lets you know exactly when you’ll hit your goal — allowing you to rest easy knowing your personal finance machine is working for you.

The hard cash amount might change as you get raises, change jobs, or come into extra money. That’s fine! The important thing is that you’re saving even if it’s a small amount.

Step 4: Earn more for any emergency

Earning money for your emergency fund is going to take time. The length of time it takes depends entirely on how much you’re earning and how much you want to put away.

If you want to put away more and crush your savings goals sooner, there’s one great way to do it: Earning more money.

That’s why my team and I have worked hard to create a guide to help you earn more today:

In it, I’ve included my best strategies to:

- Create multiple income streams so you always have a consistent source of revenue.

- Start your own business and escape the 9-to-5 for good.

- Increase your income by thousands of dollars a year through side hustles like freelancing.

Download a FREE copy of the Ultimate Guide today by entering your name and email below — and start earning more for your emergency fund today.

Emergency fund: How to build your financial parachute is a post from: I Will Teach You To Be Rich.

Via Finance http://www.rssmix.com/

No comments:

Post a Comment